RBI's assessment of India's economic growth engines paints a promising picture of the country's resilience by analyzing the condition of the four drivers of economic growth -- private consumption, government consumption, investment and exports. Despite global challenges, domestic economic activity has remained robust, the analysis said.

The government's continued emphasis on infrastructure creation, coupled with an uptick in private corporate investment and buoyant business optimism, is expected to nurture a sustained revival in the investment cycle. Private consumption is likely to receive support from improved prospects for rural demand and rising consumer confidence.

Although external demand faces headwinds from global factors, India's diversified export basket and the recovery in capital flows provide some cushion. The services sector, the backbone of the Indian economy, continues to display strength and adaptability.

RBI's analysis suggests that India's growth story remains intact, propelled by structural drivers like improving physical infrastructure, development of world-class digital and payments technology, ease of doing business, enhanced labor force participation, and improved quality of fiscal spending.

Investment Demand

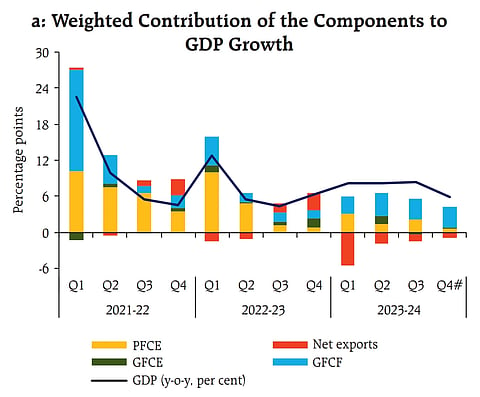

Gross Fixed Capital Formation (GFCF) grew by an impressive 10.6% year-on-year (y-o-y) in Q3:2023-24, driven by a revival in private capital expenditure (capex) and the government's continued emphasis on capital spending. The share of GFCF in GDP, although moderating slightly in Q3, achieved a new peak during the first half of the fiscal year.

Several factors contribute to the optimistic outlook for investment. Healthy balance sheets of banks and corporates, rising capacity utilization, improving business sentiment, and large public investments bode well for a sustained upturn in the private sector investment cycle. High-frequency indicators, such as the import of capital goods, production of capital goods, and construction activity, further corroborate the strength of investment demand.

The RBI also highlights the government's infrastructure push as a crucial driver of investment. The center's capital expenditure recorded a strong expansion of 28.4% y-o-y in the revised estimates for 2023-24. Moreover, the government's continued thrust on capital expenditure, as outlined in the interim union budget for 2024-25, is expected to crowd in private investment and boost productivity and growth in the economy.

Private Consumption

Growth in Private Final Consumption Expenditure (PFCE), the mainstay of aggregate demand, improved to 3.5% in Q3:2023-24 after a dip in Q2, contributing 2.2 percentage points to overall GDP growth. The RBI notes that steady urban consumption, coupled with improving income levels in the informal sector, are supporting private consumption.

High-frequency indicators of urban demand, such as domestic air passenger traffic, passenger vehicle sales, and household credit, exhibited sustained expansion in the second half of 2023-24. Consumer durables expanded at a modest pace in Q3 but recorded double-digit growth in January. Sustained buoyancy in the services sector, along with corporate salary hikes, is supporting urban demand.

Rural demand -- which has been the biggest area of concern for economists so far -- is also gaining pace gradually, as evidenced by high-frequency indicators like motorcycle sales and agriculture credit growth. The demand for work under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) declined in H2, suggesting an improvement in non-farm employment in rural areas and recovery in informal sector activity.

The RBI also highlights the improvement in labor market conditions, with the labor force participation rate (LFPR) and employment rate (ER) reflecting positive trends. The Employees' Provident Fund Organisation (EPFO) payroll data points to a strengthening of formal employment in Q3 and January 2024.

Government Consumption

Government Final Consumption Expenditure (GFCE) decelerated in the second half of 2023-24, with ongoing fiscal consolidation and expenditure rationalization. However, the central government's capital outlay grew by a robust 65.1% y-o-y during Q3, reflecting the continued emphasis on infrastructure building.

The RBI report highlights the central government's fiscal prudence while supporting growth through capital expenditure. The interim union budget for 2024-25 projects a reduction in the gross fiscal deficit (GFD) to 5.1% of GDP, marking a drop of 70 basis points from 2023-24 (RE). This is in line with the medium-term GFD target of 4.5% by 2025-26.

State governments have also continued with fiscal prudence while supporting growth with a focus on capital expenditure. The quality of states' expenditure continued to improve, owing to sustained growth-inducing capex. The RBI notes that the impact of a lower fiscal impulse on growth could be offset by higher growth-inducing capital expenditure.

External Demand

India's external demand exhibited signs of recovery in the second half of 2023-24 (October-February) despite protracted geopolitical tensions. Merchandise exports expanded by 3.7% during this period, while merchandise imports inched up by 2.5%. The recovery in merchandise exports was led by engineering goods, electronic goods, drugs and pharmaceuticals, iron ore, and cotton yarn.

Services trade, however, witnessed some slowdown in the second half (October-February) on a y-o-y basis, reflecting sluggish global demand. Services exports expanded by 5.2% in Q3, mainly driven by software, business, and travel services. On the other hand, services imports contracted by 4.3% in Q3, registering a decline for the second consecutive quarter on a y-o-y basis, primarily on account of a decline in transportation and business services.

The current account deficit (CAD) narrowed marginally to 1.2% of GDP in Q3:2023-24 from 1.3% in Q2, with an improvement in net services trade and an increase in net transfer receipts. The RBI report also highlights the sharp increase in capital flows in H2:2023-24, supported by robust foreign direct investment (FDI) and foreign portfolio investment (FPI) flows.

Services Sector

The RBI report emphasizes the pivotal role of the services sector, which contributes over 70% to GVA growth. The sector maintained its momentum in the second half of 2023-24, with an impetus from construction activity; trade, hotels, transport, communication, and broadcasting; and financial, real estate, and professional services.

High-frequency indicators suggest strong construction activity in H2, with robust growth in steel consumption and healthy expansion in cement production. The growth of trade, hotels, transport, and communication was supported by robust domestic trading activity, as reflected in GST collections.

Financial, real estate, and professional services were a major contributor to both service sector GVA growth (31.9%) and aggregate GVA growth (22.0%) in Q3:2023-24. Bank credit and deposits expanded y-o-y, and insurance premium growth in both life and non-life segments remained healthy in H2 (October-February).

The RBI report also highlights the strengthening of real estate activity in Q3, marked by the highest units sold since 2013-14. The rise in all-India housing prices remained moderate in Q3.